Your trade license is approved. You paid for it, the company is registered, and you assumed the bank account would be the simple part. Then the bank stops replying. Or it asks for a tenth document. Or it quietly declines, without telling you why.

If that sounds familiar, you are not doing anything wrong. You have hit the part of setting up in Dubai that few people explain properly. A business bank account in Dubai is a separate compliance process, not an automatic reward for holding a license. Banks here run their own checks, and they decline applications that do not convince them.

This guide is built from what actually happens inside those applications. It covers the documents UAE banks require, the real reasons applications get rejected, how long approval takes for different business profiles, the minimum balances to expect, and how to present your company so a bank says yes. There are no “guaranteed approval” promises here, because no honest adviser can make one. Just what works, and what does not.

In short: the quick answers

| Your question | The short answer |

| Can a non-resident open one? | Yes. But at least one signatory usually needs a UAE residency visa, and the checks run deeper. |

| What causes most rejections? | A transaction story that does not match the licensed activity, or an unclear owner or source of funds. |

| How long does it take? | Two to four weeks for a clean, resident-owned, low-risk profile. Six to twelve weeks for complex or higher-risk cases. |

| What minimum balance is realistic? | Often AED 10,000 to AED 50,000 for free zone profiles, and AED 50,000 to AED 150,000 or more for many mainland accounts. |

| Can you skip the bank? | An EMI or fintech account can work as an interim step, but it is not a full replacement for a UAE bank account. |

What Is a Business Bank Account in Dubai, and Why Your Trade License Does Not Guarantee One

Opening a business bank account in Dubai isn’t just a formality; it’s a strategic move that underpins your company’s success and credibility in the UAE and internationally. The benefits extend far beyond simple transaction processing

Direct answer

A business bank account in Dubai is a corporate account held by a UAE-licensed company and used to receive client payments, pay suppliers, and run payroll. Holding a valid trade license does not guarantee one. Every UAE bank runs its own compliance review and can decline a licensed company it considers high-risk.

This is the single biggest misconception in the market. Many founders believe that once the license is issued, the account follows automatically. It does not. Licensing and banking are two separate approvals, run by two separate parties, against two different sets of rules. The licensing authority confirms that your company may legally exist and trade. The bank decides, independently, whether it wants your company as a customer.

That gap widened over the past few years. The UAE rebuilt its anti-money-laundering framework and, on 23 February 2024, was removed from the Financial Action Task Force list of jurisdictions under increased monitoring, the so-called grey list (see FATF). Getting off that list required UAE banks to apply stricter customer due diligence, sharper risk scoring, and deeper checks on company owners. Those checks did not relax after the delisting. They are now standard. The Central Bank of the UAE sets the anti-money-laundering and counter-terrorist-financing rules that every bank must follow.

So when a bank asks for more documents, or questions your activity, it is not being difficult. It is doing what the regulator requires. The practical takeaway: do not treat the bank account as a formality. Treat it as a second application, and prepare for it with the same seriousness you gave the license.

Why Do Business Bank Account Applications Get Rejected in Dubai?

Applications are rejected when the bank cannot build a clear, believable picture of who you are, what your company does, and where the money will come from. In practice, not every company is approved by the first bank it applies to. For higher-risk profiles, a second-bank strategy is now normal. Four causes account for most rejections.

The transaction flow does not match the declared activity

Banks compare what your license says you do against the money they expect to move through the account. When those two do not line up, the application stalls. One recent case: a Dubai mainland IT consultancy owned by a Pakistani shareholder was rejected by an international bank because the projected transaction flow did not match the declared activity, and the company had no supplier agreements yet. The fix was not to argue. It was to revise the activity wording, add contracts and invoices that evidenced real trade, and re-present the application. The account was approved at another local UAE bank within about three weeks.

The UBO chain or source of funds is unclear

Banks must identify every Ultimate Beneficial Owner, the real person who ultimately owns or controls the company. UAE rules on beneficial ownership are set out in Cabinet Decision No. 58 of 2020 (see UAE legislation portal). When ownership is layered across several countries, or signing authority is tangled, verification slows down and confidence drops. One e-commerce company with three shareholders in three different countries was delayed because the UBO chain was unclear and the bank could not verify the source of funds quickly enough. After the ownership documentation was restructured and signing authority simplified, the account was approved.

The business activity is treated as high-risk

Some activities trigger enhanced due diligence regardless of how clean the paperwork is. Crypto-adjacent businesses are increasingly flagged even when the license itself is perfectly legal. General trading with a wide, unfocused product list, forex and payment-processing structures, and high-cash-flow models all draw extra scrutiny. For these profiles, founders are often approved only after routing initial operations through an EMI or payment solution, then applying to a traditional bank later with a track record behind them.

The company has no economic substance

UAE banks are far stricter on substance than they were a few years ago. An empty-shell company, with no office, no staff, no website, and no real operations, is hard to bank now. The bank is asking a simple question: is this a genuine business, or just a registered name? Demonstrating real presence, even a flexi-desk and an active website to start, changes how the application is read.

The pattern behind all four

A bank is not buying your license. It is buying a believable commercial story. Every rejection above comes down to the same thing: the story did not hold together. The rest of this guide is about making it hold together.

Not Sure Which Bank Will Actually Approve Your Application?

Most rejections are not about the documents. They are about applying to the wrong bank with the wrong story. Best Solution matches your profile to the right bank before you submit, so you are not spending weeks on an application that was never going to work.

What Documents Are Required to Open a Business Bank Account in Dubai?

Banks need documents that prove three things: the company is legally formed, the people behind it are who they say they are, and the business activity is real. The exact list varies by bank, company structure, and activity, but a standard set applies to almost every application. Being well prepared here is the difference between a smooth review and weeks of back-and-forth.

Core documents every bank expects

- Valid trade license issued by the relevant authority, such as the Department of Economy and Tourism for mainland companies or the relevant free zone authority.

- Certificate of incorporation or registration proving the company is legally formed.

- Memorandum and Articles of Association (MOA/AOA) setting out the company’s constitution and ownership.

- Share certificates documenting the ownership split.

- Board resolution authorising the account opening and naming the signatories. Banks usually provide a template.

- Passport copies for all shareholders and signatories.

- Emirates ID and visa copies for UAE-resident shareholders and signatories.

- Proof of address for shareholders and signatories, and an office lease, an Ejari certificate for mainland companies or a free zone lease, for the company itself.

Additional documents banks request for closer review

For newer companies, higher-risk activities, or complex ownership, banks commonly ask for more. Having these ready in advance shortens the review.

- Bank reference letters from existing personal or corporate accounts of the shareholders.

- CVs or professional profiles of the shareholders, showing relevant business background.

- Supplier or customer contracts and invoices to substantiate that the business activity is real.

- UBO declaration formally identifying the Ultimate Beneficial Owners.

Source of funds declaration explaining the origin of initial capital and expected incoming transactions.

Extra requirements for non-resident shareholders

If a shareholder or the parent company is based outside the UAE, expect additional steps. Corporate documents issued abroad usually need attestation or legalisation before a UAE bank will accept them, and that process can take several weeks and carries a fee per document. Some banks also ask for notarised passport copies and proof of address from the country of residence. For many foreign founders, this is one reason incorporating directly in a UAE free zone is simpler than running a foreign branch.

How to Open a Business Bank Account in Dubai: The Step-by-Step Process

Banks vary in their internal steps, but the core process is consistent. Knowing the sequence helps you prepare in the right order and avoid the delays that come from doing things out of turn.

Step 1: Match your business profile to the right bank

Before you touch an application form, decide which bank actually fits. SME focus, international transfer strength, industry experience, fees, and minimum balance all vary widely. Applying to the wrong bank is a common, avoidable cause of rejection. A bank that rarely banks your nationality or your activity is unlikely to start with your application.

Step 2: Prepare a compliance-ready document set

Gather every document from the lists above, and make sure the story they tell is consistent. The activity on your license, the description in your company profile, the contracts you attach, and the source-of-funds declaration must all point in the same direction. One inconsistency is enough to trigger a query and add weeks.

Step 3: Submit the application and complete KYC

You complete the bank’s corporate account opening form and submit it with the supporting documents. The bank then runs its Know Your Customer and anti-money-laundering checks. This is the most time-consuming stage. The bank verifies identities, checks names against international watchlists, assesses the risk profile of the company and its owners, and reviews the expected transaction volumes.

Step 4: Respond to bank queries and the interview

Most applications generate at least one round of follow-up questions. Some banks also require an in-person or video interview with the signatories, especially for new companies or complex structures. Prompt, accurate, consistent responses keep the application moving. Slow or contradictory answers are a common reason a review stalls.

Step 5: Activate and fund the account

Once due diligence is complete and the bank is satisfied, the account is approved. You receive your IBAN, account number, and online banking details, and you make the initial deposit required to activate the account. The welcome kit, cheque book, cards, and security tokens follow. Only now is the account ready for live operations.

Choosing the Right Bank: Local Banks, International Banks, and EMI Alternatives

There is no single best bank for a business account in Dubai. The right choice depends on your nationality, your activity, your transaction pattern, and how much balance you can realistically hold. Three categories are worth understanding.

| Option | Examples | Best suited to |

| Local UAE banks | Emirates NBD, Mashreq, ADCB, RAKBANK, Dubai Islamic Bank, FAB | Companies trading mainly in the UAE; SMEs wanting branch access and local relationship managers |

| International banks | HSBC, Standard Chartered, Citibank | Businesses with significant cross-border trade and existing global banking relationships; usually higher thresholds |

| EMIs and fintech platforms | UAE-licensed and international electronic money institutions | International founders needing a fast, multi-currency interim account before a full traditional bank |

Local UAE banks

Local banks tend to have wider branch networks, a deeper feel for the local market, and SME-focused packages. They are often the most workable choice for companies whose trade is mainly inside the UAE. They still apply full due diligence, but a local relationship manager who understands your profile can be a real advantage.

International banks

International banks offer strong global networks, which helps businesses with heavy international trade. They often expect higher minimum balances and apply stricter criteria, so they suit established companies more than first-time startups.

EMIs and fintech platforms as an interim option

An Electronic Money Institution, or EMI, is a regulated provider that offers multi-currency accounts and payment services without being a full bank. EMIs typically onboard faster than traditional banks and ask for fewer minimum-balance commitments, which makes them a practical interim solution for international founders. They are increasingly used as a first step, with the company moving to a traditional UAE bank later once it has a transaction history. An EMI is not a full replacement: some local services and the depth of a full banking relationship still sit with traditional banks. Used in sequence, though, an EMI can keep a business operating while the bank application runs.

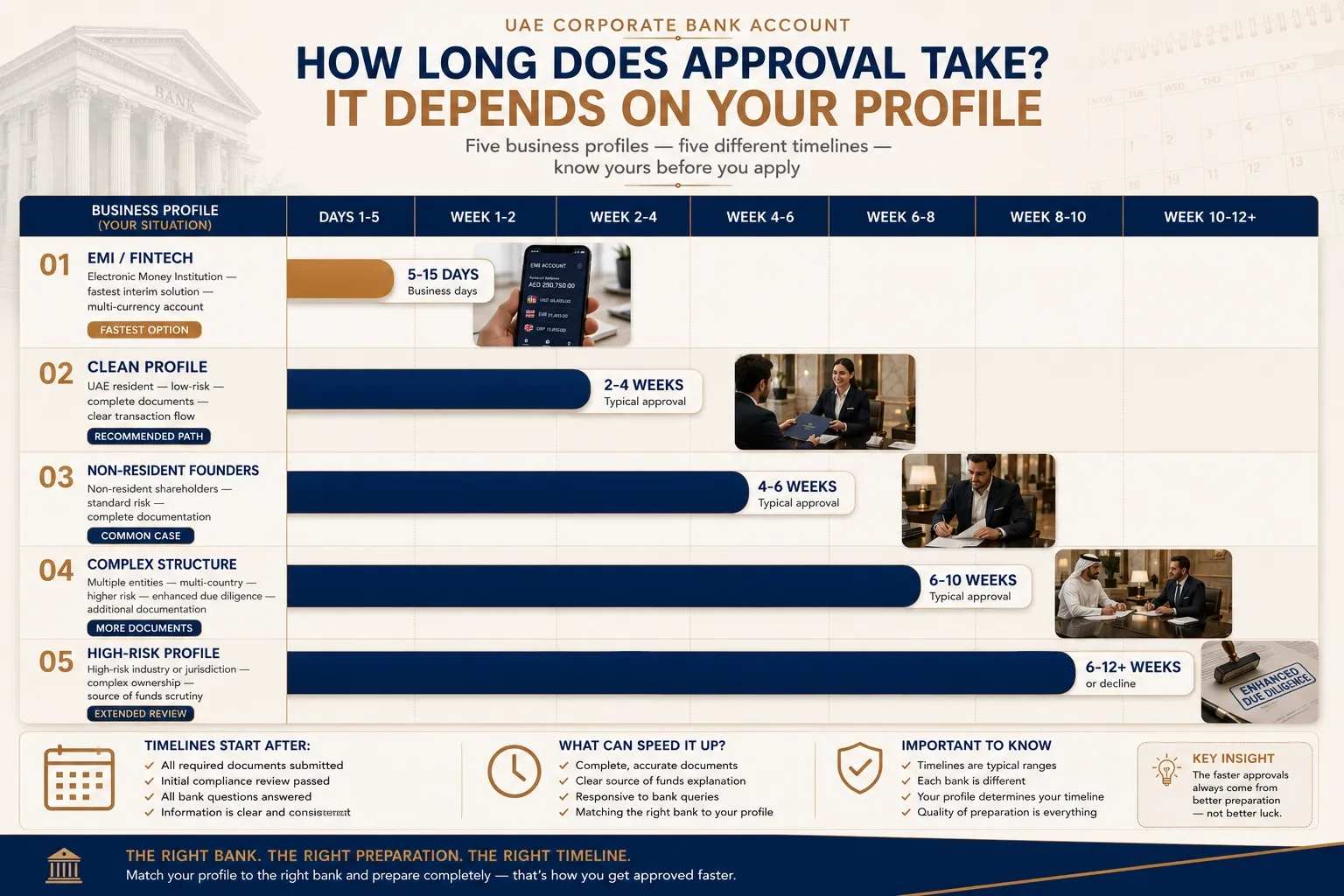

How Long Does It Take, and What Will It Cost?

The honest answer to how long it takes is that it depends on your profile. The honest answer to what it costs is that the headline fees matter less than the balance you must maintain. Here is what to plan for.

Realistic timelines by business profile

| Business profile | Typical timeline to an active account |

| Low-risk, UAE resident-owned, complete documents | 2 to 4 weeks |

| Non-resident founders or shareholders | 4 to 8 weeks |

| Complex or multi-country ownership | 8 to 12 weeks |

| High-risk activity (crypto, broad general trading, payments) | 6 to 12 weeks, or a decline |

| EMI or fintech alternative | Often 5 to 15 business days |

The fastest approvals share a pattern. They tend to come from companies that already have UAE residency for a signatory, local address proof, an active website, contracts or invoices in hand, and a clear transaction flow. Missing or inconsistent documents are the most common reason a timeline doubles.

Minimum balance and fees to expect

Minimum balance is usually the real cost of a UAE business account, not the opening fee. It varies sharply by bank and by profile. Free zone company accounts often sit in the AED 10,000 to AED 50,000 range, while many mainland accounts expect AED 50,000 to AED 150,000 or more. Premium accounts and non-resident-owned companies can be higher again. Fall below the required balance and the bank charges a monthly penalty. Also budget for monthly maintenance fees, transfer charges, and currency-conversion costs.

One practical point that surprises many founders: the official minimum balance and the expected balance are not always the same number. Relationship managers often discuss an informally expected balance, the level at which they are comfortable with the relationship, even when the published minimum looks lower. It is worth asking that question directly before you choose a bank.

Mainland, Free Zone, and Offshore: How Your Company Type Affects Banking

Your company structure shapes how the banking process runs. A mainland company , registered with the Department of Economy and Tourism, has full access to the UAE market and goes through standard due diligence, though it often faces higher minimum balances. A free zone company, set up in a zone such as DMCC, IFZA, or JAFZA, allows full foreign ownership and can sometimes access lower balance thresholds through free-zone-friendly banking teams. An offshore company, such as a RAK ICC or JAFZA Offshore entity, is the hardest to bank: due diligence is stricter, balance requirements are higher, and some banks decline offshore accounts altogether.

The structure you choose for licensing cost alone can quietly cost you at the banking stage. It is worth weighing the real cost of starting a business in Dubai with banking in mind, not just the license fee. The certificate of incorporation and related formation documents you receive at setup are the same documents the bank will scrutinise later.

How to Improve Your Approval Chances

The biggest mistake founders make is choosing business activities and a company structure for licensing cost alone, without thinking about banking impact. Combining unrelated activities, using a broad general trading structure with no real transaction explanation, applying before you have invoices, contracts, or a website, and using nominee shareholding structures that add compliance risk all make the bank’s job harder. A bank wants a believable commercial story, not just a valid license.

These steps consistently improve the odds:

- Narrow your business activities to what you will actually do, so the license matches reality.

- Simplify ownership and signing authority a clear UBO chain verifies far faster than a layered one.

- Demonstrate real economic substance an office or flexi-desk, staff, and an active website.

- Bring contracts and invoices early evidence of real trade answers the bank’s main question before it is asked.

- Keep one consistent transaction narrative the license, profile, contracts, and source-of-funds declaration must agree.

- Consider starting with an EMI if you are an international founder, build a track record, then apply to a traditional bank.

- Be ready for a second-bank strategy one rejection is not the end; the right second application often succeeds.

How Best Solution Helps You Open a Business Bank Account in Dubai

Best Solution has operated in the UAE since 2014 and has handled thousands of company formations and related banking-support cases across mainland and free zones. The team, including CEO Essa Al Harthi and Managing Director Vipin Kumar, advises clients on setup and banking readiness based on real application outcomes, not theoretical requirements.

It is worth being clear about what business bank account assistance is, and what it is not. No consultant can guarantee an account. Banks do not allow anyone to promise approval, and any provider advertising a “100% guarantee” is selling something that does not exist. What genuine assistance does is different and, for most founders, more valuable:

- Bank matching recommending banks that realistically suit your nationality, activity, and profile, so you do not waste weeks on the wrong application.

- Compliance positioning framing your activity and ownership so the bank sees a clear, believable commercial story.

- Document preparation compiling a consistent, complete document set that meets UAE banks’ standards the first time.

- Application follow-up and query handling managing the back-and-forth with the bank and helping you answer queries quickly and accurately.

- A second-bank strategy if one bank declines, moving fast to the right alternative instead of starting from zero.

A recent example shows how this works in practice. A free zone marketing consultancy, founded by an Indian entrepreneur with overseas clients, was first rejected because the projected turnover and the founder’s personal profile did not align with the bank’s expected activity. The application was rebuilt with a revised business plan, a proper transaction forecast, supporting contracts, and a clearer explanation of inbound international payments. The account was approved at a UAE local bank roughly 10 to 14 working days after resubmission, and the client later scaled into multi-currency operations.

Before you apply, make sure you have

Opening a business bank account in Dubai rewards preparation. Treat it as a second application, tell one consistent commercial story across every document, choose the right bank before you apply, and keep a backup in mind. Do that, and the process moves from an anxious unknown to a predictable step.